Today’s newsletter is a guest contribution from Drew Cashmore, the chief strategy officer at ad-tech firm Vantage. As someone involved in the early days of Walmart Connect, Drew has a unique vantage point (get it?!) in the ecosytem, and his newsletter, Retail Media Leapfrog, is a must-follow.

This piece was originally published as Retail Media Leapfrog Series: The Fermi Paradox on April 1, 2026, by Drew Cashmore. Please enjoy!

"Where is everybody?" asks Tim Urban in one of my favorite blog posts of all time.

For those not familiar with the 'Fermi Paradox', it goes something like this:

A conservative estimate suggests that there should be 1,000,000,000 habitable planets, and 100,000 intelligent civilizations in our galaxy alone. So why haven't we seen any intelligent life?

The Fermi Paradox highlights the contradiction between the probability of extraterrestrial life, and the lack of evidence of its existence. It centers on something called the 'great filter', and suggests that there are a few potential reasons for this:

- No higher civilizations exist: Intelligent life on earth is an infinitely impossible fluke. We are rare. The move from single to multicellular organisms, as one example, is rarely surpassed.

- The 'great filter' is in our not-so-distant future: most civilizations don't advance much beyond our point. Either we create technologies that inadvertently destroy ourselves (good thing we're definitely not on that path...), or most civilizations see some other type of cataclysmic event.

- Other Logical Reasons: we might be too primitive to see it (like an ant on the side of a four-lane highway), or maybe other civilizations are content with staying in one place?

Now - to draw an unnecessary parallel to the much less consequential thing I spend most of my life on - I give you, Retail Media's Fermi Paradox:

A conservative estimate suggests that there are 95 retailers globally, that carry predominantly national brands, and generate over $10BN in revenues. If you assume an individual retailer can capture 1% of its sales in retail media investments, why don't we have more $100M+ retail media businesses? Why don't we have more $50M+ retail media businesses?

Source: List of largest [global] retail companies

The Retail Media Fermi Paradox highlights the contradiction between the value that many global retailers drive for their supplier base, and the lack of share capture of those supplier's marketing investments.

SPONSOR: MIRAKL ADS

Retailers know that a marketplace model can dramatically boost product assortment, shopper engagement, and total revenue.

But, to get the most out of your marketplace, you need an ad tech solution that can really engage sellers.

Mirakl Ads is powering the future of retail media for leading retailers — to activate both 3P sellers and 1P brands.

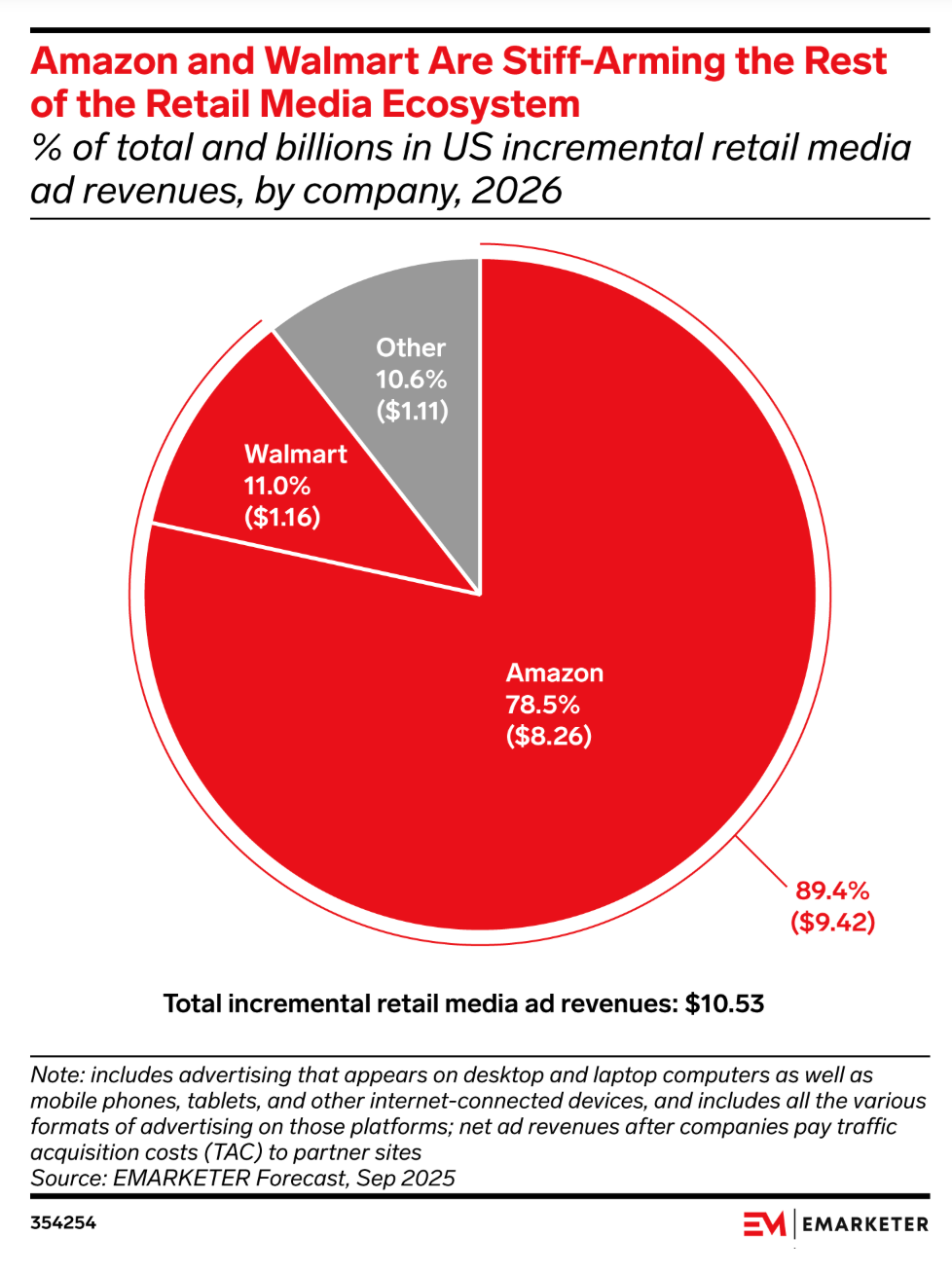

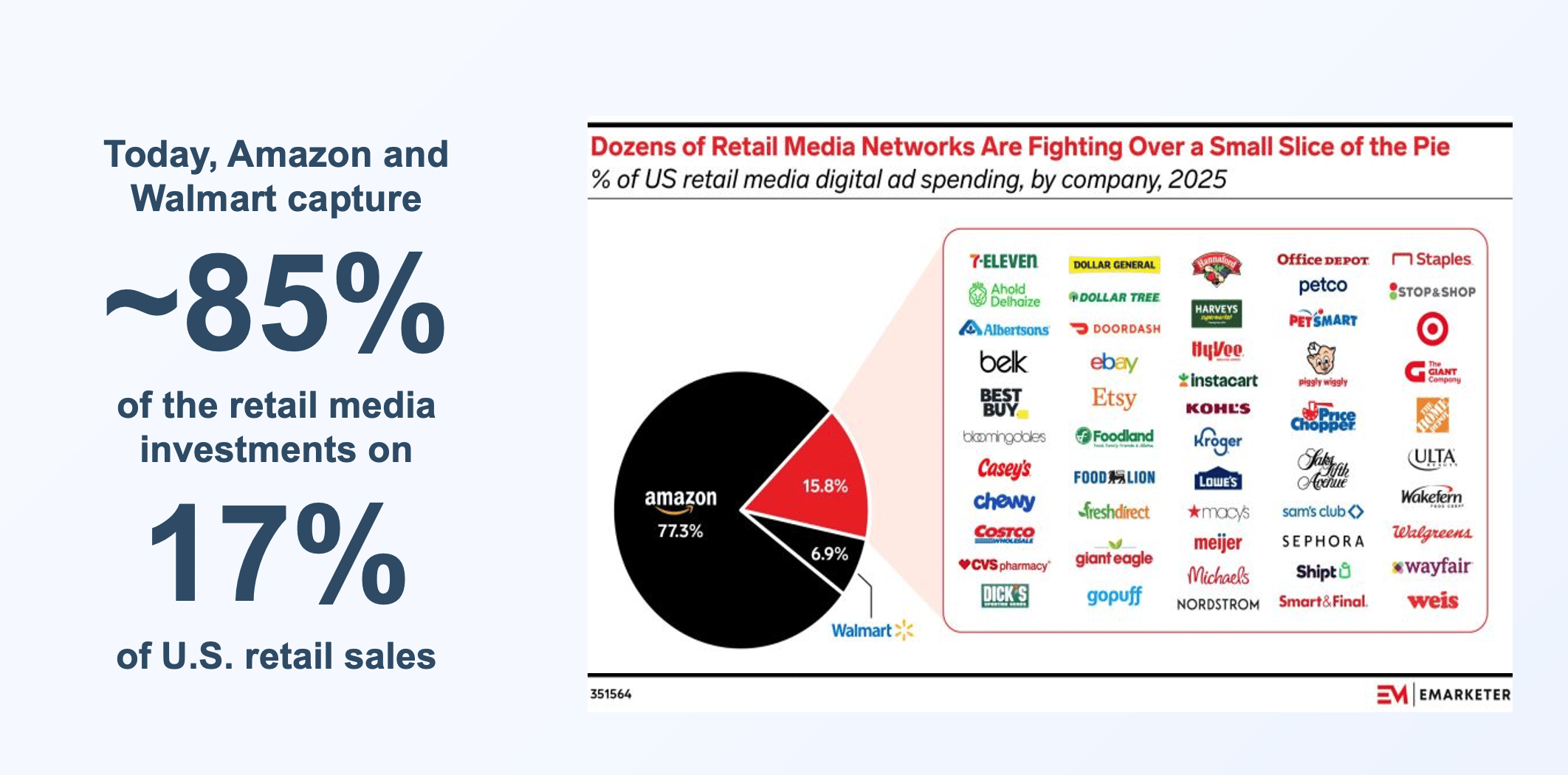

You've probably seen Max Willens' and Sarah Marzano's charts - Amazon and Walmart will collectively capture about 90% of retail media investments in the U.S. market moving forward - up from their current dominance of 85%. Slightly less-so for Europe but still incredibly high.

This is to say, retail media is massive, but revenues are consolidated at the top.

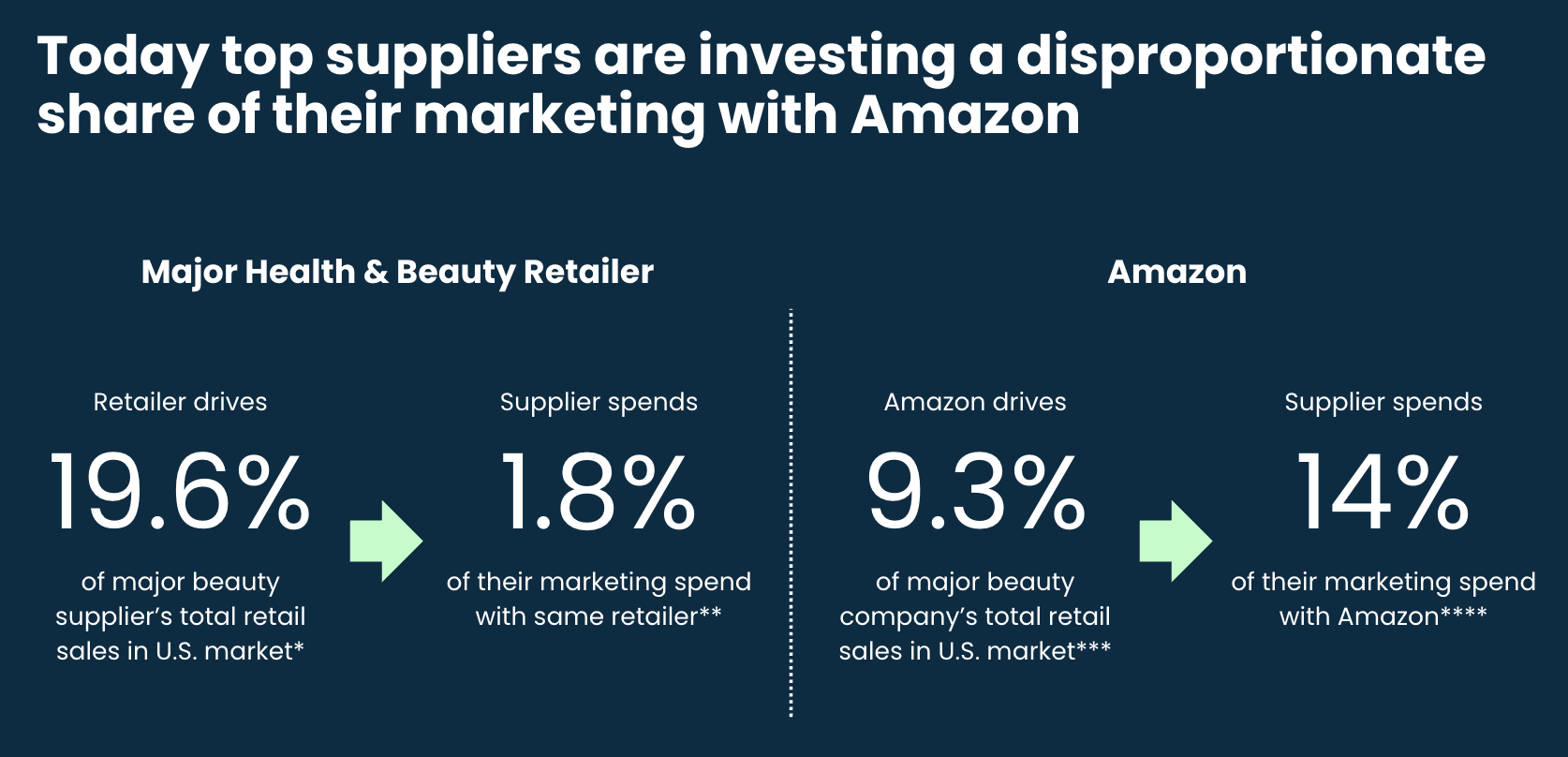

If you drill it down into individual retailers, you can often see category dominant retailers losing retail media investments to Amazon in spite of those retailers having a disproportionate share of retail sales for their supplier base.

That's not cool!

In this weeks Retail Media Leapfrog Series - posts that help to inspire next generation retail media businesses to leapfrog incumbents - we're going to chat about about the 11% of the pie (that non-Amazon and Walmart piece), why it is so small today, and how we can make it bigger.

And to do that, we're going to first look at some of retail media's great filters today:

Great Filter #1: The Tactic Trap

Amazon and Walmart own ~85% of the $70BN in retail media investments in the U.S. market. But what percentage of retail do they represent?

17%. Amazon and Walmart collectively capture about 17% of U.S. retail consumer spending. (Source)

I cannot make that number big enough! In fact, maybe it's just better to visualize it:

Zoom in and it tells a slightly different story. Amazon and Walmart capture roughly 50% of all U.S. retail consumer spending online. (Source).

Guess where retail media ads predominantly show up?

According to data from Andreas Reiffen and Pentaleap, about 64% of ad spend in retail media is coming from onsite product listing ads. Another 20% is coming from onsite display.

84% of retail media ad investments happen on retailer websites.

The greatest trick that Amazon ever pulled was convincing retail media buyers that retail media should be mostly product listing ads.

Walmart followed suit, and rest of market has been chasing this ever since.

What this means is that most retailers are attempting to win share against two players that dominate both the sales and maturity of technology, in the tactical areas where these ads appear.

To put it plainly, Amazon and Walmart are really good at product listing ads, and have a massively scaled ecosystem to support those efforts.

Great Filter #1: copying the Amazon playbook, competing on their turf.

Great Filter #2: The Investment Trap

Kiri Masters has coined the next great filter. Writing in The Drum, she describes how mid-tier networks are caught in a 'doom loop'. "Without revenue they can't invest in technology, without technology they can't attract revenue."

It's a vicious cycle that is entirely self-inflicted.

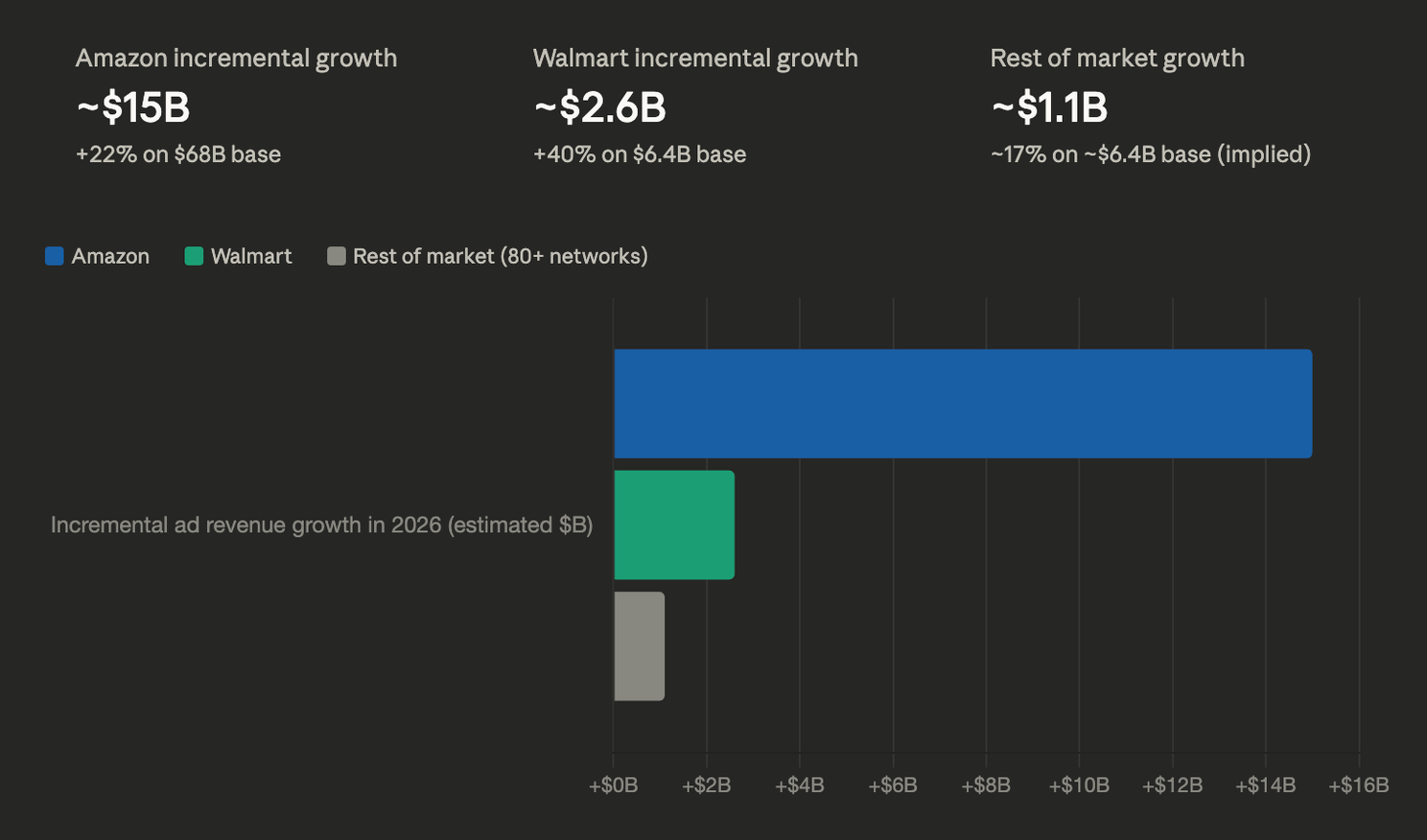

Growth is decelerating too according to EMARKETER - from 26% YoY growth in 2024 (source), to 17.9% YoY in 2026 (source) - with rest-of-market growing at a slower percentage rate than Amazon and Walmart, despite their size.

The retailers who were going to win on momentum or scale alone have already won. Everyone else is now competing on merit - and merit requires investment.

Which brings us to the real Great Filter #2: low to no investment in growth.

Amazon and Walmart invested hundreds of millions, if not billions, over the past 15 years. They invested in retail media, independent of its growth at the time in:

- Technology

- People

- Go-to-Market

- Change Management

And it clearly worked.

But many retailers have never made a strategic investment in this business. Many launched retail media networks in name only, with minimum viable investment or investment off a small percentage of retail media revenue.

Sarah Marzano has been saying this for a while, "Retailers and their retail media teams need to start thinking about playing the long game," she's argued - pointing out that the retailers failing aren't failing because the opportunity isn't real, they're failing because they're treating a transformation like a bolt-on revenue line.

James Bauer put it best, "you get out of this industry what you put into it".

Great Filter #3: The Commodity Trap

Most retailers have something genuinely valuable and unique - real purchase data at scale, tied to real audiences. It's the reason why Retail Media exists at all.

And it's something most media companies can only extrapolate.

But, as I said in Pesach Lattin's incredible and massive report on retail media, 'Many retailers [are starting to] ship their data to third parties to sell it on their behalf. This approach commoditizes the value of first-party data overall, returning pennies on the dollar while retailers lose control of their most strategic asset. The short-term revenue feels good; the long-term erosion of differentiation doesn't show up until it's too late'.

The thing that made retailer data different is suddenly accessible to anyone.

And that ultimately leads to a commoditization of the value of retail media overall.

But what makes it worse is the loss of a direct relationship with your advertiser (your suppliers). For retailers that own that direct relationship on the merchandising side, it might be unfathomable that you would outsource your buying, pricing and even the visibility of outcomes to a third party to manage in the background - but that is what is happening in retail media.

Your data might not be co-mingled with other retailer data, but from a buying perspective, your signals are very similar to everyone else.

The Wise Marketer Group put it plainly: "RMNs are beginning to reckon with the reality that they've given away their competitive advantage and enabled their own disintermediation - as platforms offer comparable data quality at lower prices."

And if you've already ceded the relationship, it will get incrementally harder to regain those relationships as time goes on.

Great Filter #3: your data and access is only differentiated if it's yours. The moment someone else can buy around you, you've lost control.

Great Filter #4: The Fragmentation Trap

At Shoptalk this year, Christine Foster said, "There is still a lot of friction in scale and interoperability - marketers want to reach audiences wherever the are, and that’s not always easy to do".

I concur.

The retail media tech stack is impossibly complex, and it's creating a lot of decision fatigue for procurement teams.

But more importantly it means that today,

- Retail media is really hard to buy

- Retail media is really hard to operate

- Retail media is really hard to measure

RMIQ and Skai have some amazing data on this:

- $28 billion in industry-wide revenue loss attributable to fragmentation (on a $70BN industry!!)

- Enterprise brands spending $10M+ annually require 6-10+ FTEs organized as full departments with specialized roles across 12+ retail media networks.

Growth today often only comes from throwing people at the problem. And unfortunately in most retail organizations today, that is not longer an option.

But this challenge isn't just an oversight. I love Mark Williamson's transparency here in a recent Kiri Masters's article, "I've been one of those people that's been insecure about my platform. I've been ignorant of my technology partners. And that does put you at a disadvantage when you're trying to have a JBP conversation with a supplier, or you're talking with an agency and you just don't feel confident in your stuff."

To me this says that technology has not always been at the forefront of what we're building here - and that the leaders in our space are often playing catchup as it relates to how to stitch this all together.

Great Filter #4: fragmented, disconnected technical architecture results in businesses that only scale by adding more people.

Breaking Past the Great Filters

Is there scale out there for rest of market?

Absolutely. I've seen it show up in a bunch of ways, but there are too many nuances to properly capture in this article.

For the sake of simplicity, I'd suggest three key paths to breaking the filter today:

Move #1: Orchestrate Outcomes (Breaks the Tactic and Fragmentation Trap)

The Tactic and Fragmentation Trap share a root cause: retailers building reactively, one piece at a time, chasing what Amazon built rather than building what only they can.

The answer to both isn't a new tactic. It's a new architecture.

Orchestrating outcomes means building retail media omni-channel by default - not as an aspiration, but as a baseline design principle. Unified front-end. Single planning workflow. Measurability built in from day one. Ad formats that work together. Buying that's as easy for your supplier as it is for your operations team to run.

All jobs-to-be-done, all in one place.

The important nuance in this is that most efforts in orchestration go only part way, leaving retailers and brands to manage efforts in multiple systems and tools, even if the initial planning functions are consolidated.

This isn't about adding more tools. It's about collapsing and connecting them.

Orchestration isn't an IT project. It's a competitive moat.

Move #2: Own Your Moat (Breaks the Commodity Trap)

First-party purchase data - or more specifically, the ability to connect ad views with purchases in the places where people shop - is the reason why retail media exists. Direct supplier relationships are the reason it compounds.

Don't give either away.

Owning your moat means keeping your data inside your own environment and/or in a way that allows you to keep control of the outcomes and usage. And it means maintaining a direct commercial relationship with your advertising partners - because the moment someone else manages that relationship, they become the retailer.

Costco's approach here is strong. Mark Williamson set three non-negotiables from day one: own the data, minimize data movement, minimize data copying.

The window to reclaim this is open. But every quarter you cede the relationship, it gets harder to earn back.

Move #3: Invest in Growth (Breaks the Investment Trap)

Strategic investment in retail media isn't a line item inside retail media revenue. It's a capital allocation decision - the same kind of decision made for a new store, a new distribution centre, or a new ERP. Technology. People. Go-to-market. Change management.

A while back I wrote an article called 'The Economics of Waiting' about the compounding effects of inaction. What I framed in that article was part of the business case - one centred on the IRR and NPV value of the business among other things. Essentially, how do you talk to your CFO about retail media investments against all other retail priorities.

Amazon and Walmart didn't build billion dollar retail media businesses by growing at market pace. They invested ahead of the curve - in infrastructure and talent that made scale possible. The compounding effect of that investment is exactly what makes the rest of market's position harder every quarter.

This is not a side business for retail anymore, it is a strategic priority.

Move #4: Chase Mutual Value (Breaks the Investment Trap)

Stefanie Jay - the visionary behind Walmart Connect's meteoric acceleration - used to say: "When you grow, we grow. When we grow, you grow."

It sounds obvious, but isn't always practiced.

The commercial model that chases extraction - treating retail media as a fee for access or a profitability lever to be pulled - will always underperform the model that chases mutual value. And advertisers can tell the difference. They've been trained to by Amazon to expect something in return for investment.

I've written before about the shift from Trade to Retail Media as moving from defence to offence. Trade asks: what will you give me for access? Retail Media asks: what will you give me for growth? The retailers that understand this distinction - and build their commercial model around it - are the ones whose supplier relationships compound over time. More trust. More investment. More data shared. The retail media flywheel.

The ones that don't keep waking up to the same conversation: why are our suppliers spending more with Amazon?

Because Amazon proved it was worth it.

Mutual value isn't just a philosophy - it's an operating model. It means joint planning with your suppliers, not just selling them inventory. It means measurement that proves incrementally and/or some other intrinsic value shared with your suppliers. It means your retail media team and your merchant team sharing goals, not competing for the same budget.

When retail media is truly mutual, it stops being a media business and starts being a growth business. For everyone.

That's the leapfrog.

Closing

The Fermi Paradox offers a grim hypothesis: most civilizations don't make it through the great filter. But the reasons for this are often outside of any civilizations control (unless they build technology that reaches the singularity - but no one is crazy enough to do that)!

In Retail Media's Fermi Paradox, the great filters are almost entirely behavioural. And behaviour can change.

The 11% that isn't Amazon and Walmart doesn't have to stay 11%. The audiences are there. The purchase data is there. The supplier relationships are there. The technology to orchestrate it all - to own your data, build unified infrastructure, and invest for mutual growth - exists today in a way it simply didn't five years ago.

The leap is possible. We know because we've seen it happen. The retailers that invested ahead of the curve, protected their moat, and treated retail media like the business it is are winning.

That's what the Leapfrog Series is about. The path has been walked. The lessons are documented. The question is whether you'll run the playbook while the window is still open?

If you're sitting inside one of these filters right now - I'd love to hear from you and would be more than happy to chat through it.

Subscribe to the series. Share this if it resonated. And as always - comment, debate, push back. That's how we all get smarter.

Thanks Drew for contributing this piece to Retail Media Breakfast Club. You can read the original essay here — and enjoy the smart conversation that also unfolded in the comments section.