Last week I hosted a LinkedIn Live all about in-store retail media, and if we are measuring the right things.

Paul Brenner, SVP of Global Retail Media & Partnerships at In-Store Marketplace, and Michelle Dooley, Founder of Catalyst Media, joined me to discuss new research they've collaborated on — and its central argument is that we've been measuring in-store retail media with the wrong scorecard entirely.

Their thesis: digital in-store has borrowed its measurement model from online media, chasing one-to-one attribution in an environment where it doesn't fit. The result is that most in-store digital investments are stuck in test budgets, never graduating to annualized spend. Here's what stood out from the conversation.

I asked: Why is measurement the barrier — and why now?

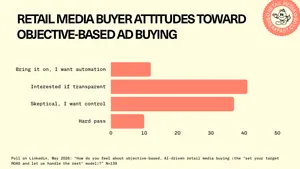

Michelle explained that when they started interviewing CPGs, RMNs, and agencies across the US and Europe, they expected to hear that measurement needed to be more sophisticated. Instead, they heard something more basic: people couldn't even agree on what "in-store media" meant. Brands and merchants think of in-store as everything — end caps, shelf talkers, print signage — not just digital screens. And the way success gets judged depends entirely on who you ask.

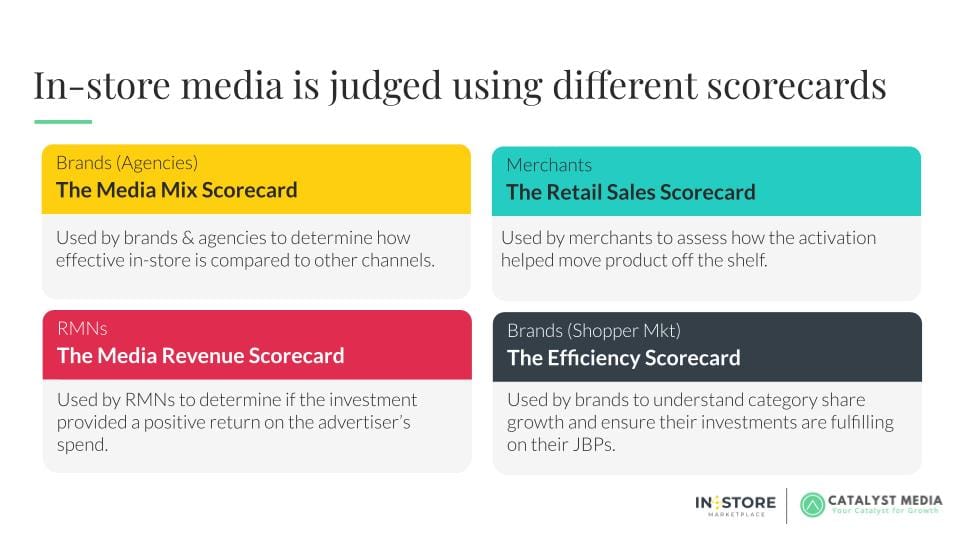

That led to the insight: in-store media is being evaluated against four competing scorecards simultaneously. Brands and agencies judge it on media mix performance. Merchants judge it on product movement. RMNs judge it on media revenue. And shopper marketing teams judge it on efficiency against their JBPs. Those four groups are grading the same activity on completely different criteria — and nobody's passing.

"By focusing on the technical measurement capability gap, we've missed the measurement alignment gap," the report says.

One interviewee told Michelle that their leadership didn't have FOMO about digital in-store — because the merchant wasn't asking for it. Without a shared language between the RMN and the merchant, digital in-store stays an innovation experiment.

I asked: So what's the proposed fix?

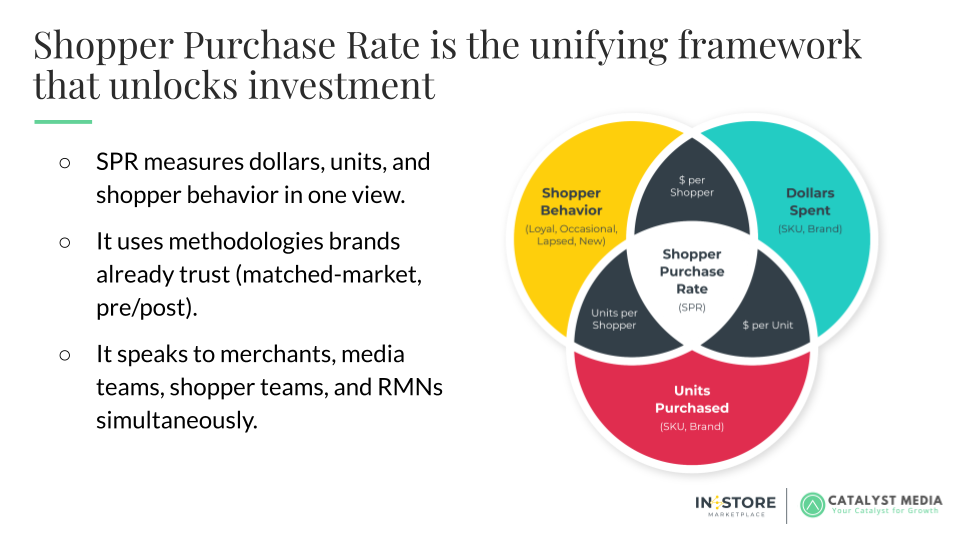

Their answer is a framework called Shopper Purchase Rate (SPR). It sits at the intersection of three things: consumer dollars spent, units purchased, and shopper behavior segmented by loyalty status — loyal, occasional, lapsed, and new-to-brand.

The key design choice is what SPR doesn't try to do. It doesn't chase one-to-one attribution. Instead, it relies on matched-market tests and pre/post analysis — methodologies that brands and merchants already trust. A pre/post test gives you SPR. A matched-market test where digital in-store is the variable gives you incremental SPR.

Michelle was candid that SPR isn't meant to replace existing metrics. A category leader will still care about matched-market dollar and unit lift. An omnichannel planner will still want iROAS. But SPR gives everyone a common baseline — a through line across those four scorecards that lets the merchant, the media team, and the brand talk about the same thing.

Michelle shared an anecdote that made the concept click. When she was at Target in the early days of what became Cartwheel, her team had to justify tens of millions in markdowns to run coupon programs. The conversation was always about cost pressure on the P&L — even when they could prove incrementality. Then a merchant-side leader rebranded "markdowns" as "shopper savings." Same dollars, completely different internal story. Suddenly, leadership was touting $94 million in shopper savings instead of agonizing over markdown expense.

That's the parallel she's drawing with SPR: the right framing changes who's willing to advocate for the investment.

Retailers know that a marketplace model can dramatically boost product assortment, shopper engagement, and total revenue. But, to get the most out of your marketplace, you need an ad tech solution that can really engage sellers. Mirakl Ads is powering the future of retail media for leading retailers — to activate both 3P sellers and 1P brands.

From the audience: Does SPR apply beyond performance campaigns?

This came from Jorn Olsen, and it's the right stress test. Michelle pointed out that digital in-store isn't always bottom-funnel — challenger brands use it for point-of-sale visibility, and some retailers are experimenting with experiential activations. But when brands go back internally to justify the spend, the conversation comes down to cases moved and bottom-line impact regardless of where the campaign sat in the funnel.

Paul added that non-endemic advertising — telco, digital payments — is still a small slice of in-store inventory, roughly 5% of fill rate heading toward 10%. Those buyers care about impressions and brand awareness, not product movement. SPR isn't really built for them, and that's fine.

From the audience: How does this translate to Europe?

Courtland Dearing asked this, and it connects to something I explored in a recent piece on why US and European in-store retail media evolved so differently. Paul has spent time embedded in the UK market, where in-store started first and the common currency has long been cost per shopper. The UK essentially absorbed shopper and trade into the RMN using product-movement metrics from the beginning — which is close to what SPR proposes for the US market.

Michelle added a useful distinction: exterior-facing screens in a retail environment behave more like digital out-of-home, measured on reach and frequency. Interior screens are where SPR adds the most value — and where matched-market tests could prove that the digital activation actually drove incremental product movement.

Where I land

The SPR framework is still early — Catalyst and ISM are heading into a validation phase with brands and RMNs who came forward after seeing the initial research. So this is a proposal, not a proven standard. But the underlying diagnosis feels right to me: the industry has been trying to make in-store digital look like online media instead of building measurement that fits how stores actually work. And the organizational insight — that you need the merchant and the media team speaking the same language before any metric can do its job — maps to patterns I keep seeing across this industry.

Paul closed us out with a line I'll leave you with: "The brand has the need and the RMN has the power."

You can watch the full livestream of this discussion here, and download the report here.

The LinkedIn Live was sponsored by In-Store Marketplace.