Taipei, December 2024. My brother, my dad, and I splurged on a stay at the Grand Hyatt before an epic bike tour down the east coast of Taiwan—one of those once-in-a-lifetime trips that justified a proper send-off. The breakfast buffet was absurd in the best way: a sushi bar, dim sum, high-end cheeses, and pastries that belonged in a Parisian bakery.

Day one, we were giddy. "You try the dim sum, I'll get the sashimi." We compared detailed notes on what was worth it, and we all went back for thirds.

By day four, we had become picky. We were more discerning about which foods were worth taking up space on our plates. We returned to our go-to favorites. We complained that the brown sugar crumb cake seemed stale today.

What had been a luxury just a couple of days before had become a baseline, an expectation.

This is the hedonic adaptation problem retail media is facing in 2026.

Early on, brands were dazzled by the promise—first-party data! closed-loop attribution! incremental sales! Budgets flowed easily.

But as retail media became an established line item, the excitement faded into expectation. What once felt like a luxury buffet now feels routine.

And when the novelty wears off, brands start asking harder questions: "Is this actually worth it?"

SPONSOR: MIRAKL ADS

With unique AI capabilities that prioritize relevance, and self-service options for every size of advertiser, Mirakl Ads is the ad-tech solution trusted by global enterprise retailers like Rakuten.

Learn about Mirakl Ads’ marketplace-ready retail media solution that supports full-funnel ad formats, tailored for both 1P and 3P marketplace sellers.

The Budget Momentum Is Fading

The Path To Purchase Institute's 2026 Retail Media Ratings study surveyed 166 CPG and agency professionals, and the headline reminds us that the gold rush is over.

Nearly 6 in 10 organizations increased their retail media investment in the past year—still a majority, but down from 70% a year ago. Only 17% plan "significant" budget increases, compared to 27% in the previous study. Meanwhile, the share reporting decreased investment rose from 16% to 21%.

This is the retail media doom loop in action. Last September, I described how retailers "launch with sky-high profit expectations, grab quick wins by repackaging trade dollars, then stall out when that easy money runs dry." Much of retail media's early growth came from reallocating existing trade and shopper marketing spend—essentially relabeling dollars, not creating new ones. Those pools have limits, and we're hitting them.

Brands now treat retail media as an established line item (on average, one-third of total marketing budgets), which means incremental dollars are harder to come by.

The Confidence Gap

The share of brands who view retail media as "just a money grab by retailers" has more than doubled—from 8% to 19%.

Sure, that’s not the majority of media buyers. But paired with another finding, it tells a story. The share who see retail media as "as effective or more effective than other digital media" dropped from 80% to 71%. That's a 9-point slide in perceived effectiveness in a single year.

To be clear, the market isn't planning a mass exodus from retail media, but it is getting more skeptical at the margins.

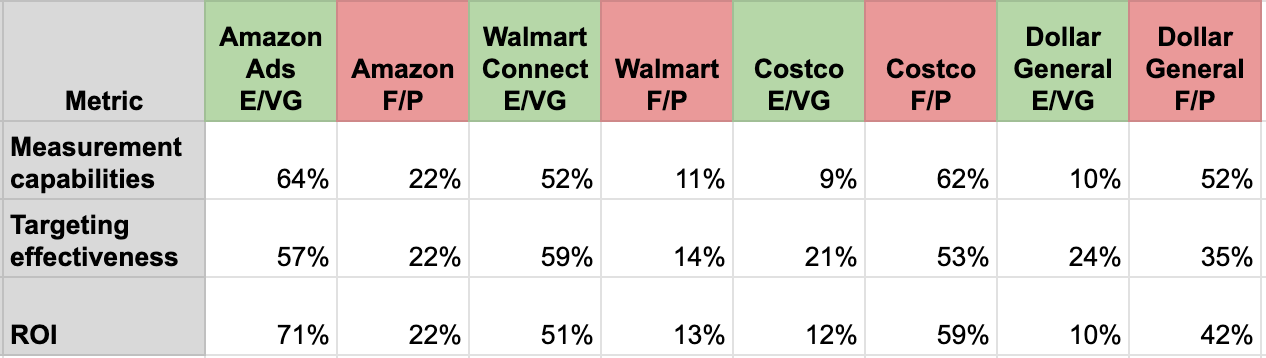

The performance hierarchy itself remains largely unchanged. Walmart Connect earned 52% "Excellent/Very Good" ratings for driving sales growth—directionally up from last year, according to the study. Amazon maintains its position at the top. Regional players and mid-tier grocers continue to trail significantly across several key metrics.

I’ve pulled out just 3 metrics out of 8 from the P2PI Ratings to show the performance differential between Amazon & Walmart, versus DGMN and Costco who are in the mid-pack. 32 RMNs were rated in the full report.

The numbers below are the % of respondents rating each network ‘Excellent/Very Good’ (E/VG) vs ‘Fair/Poor’ (F/P) for the specific metric.

Last year I wrote that the gap between top-tier and emerging RMNs had widened, based on that year’s P2PI RMN rankings. This year's data suggests that chasm has calcified. The leaders aren't pulling further ahead so much as everyone else is failing to close ground.

Respondents who held the "money grab" view cited high spend requirements, poor data transparency, and weak performance as reasons. As one CPG marketer put it: “Some retailers provide a strong experience onsite and integrate their ads thoughtfully. Other retailers feel like they are just trying to cash in.”

Measurement Remains the Dividing Line

Nearly half of media buyers (48%) in the study cite measurement and attribution as their top challenge, according to the study. That's very interesting given how often retailers publicly tout their closed-loop capabilities.

I've profiled networks that are getting it right, or at least proving that they’re willing to be accountable and invest in their capabilities: Best Buy built an attribution system where 93% of transactions tie back to a customer ID. Dollar General implemented randomized controlled trials based directly on IAB guidance. Costco just revealed their comprehensive ad-tech stack showing a big investment in a flexible data foundation.

There's a small bright spot in the P2PI data: mentions of data-sharing frustrations declined year-over-year in open-ended responses. That doesn't mean the problem is solved, but it suggests the frustration mix may be shifting—less "where's my data?" and more "prove this actually works."

Now What

For RMNs outside the top tier, the mandate is clear: investment intensity is fading, skepticism is rising, and the networks that can't demonstrate genuine value will find budgets harder to secure. The doom loop isn't inevitable, but breaking out of it requires real commitment to measurement, transparency, and infrastructure—not just new ad formats.

For brands, the takeaway is to be more selective. The data backs up what many have suspected: concentrate spend where retailers can prove they drive growth, and approach underperformers with pilot budgets and strict KPIs.

The buffet at the Grand Hyatt Taipei was legitimately excellent. But by day four, when the novelty wore off, I started running a value calculation in my head: Is this worth $50 per person?

Retail media has entered that same phase. Brands are no longer dazzled by the promise of first-party data and closed-loop attribution—they're asking whether the premium is justified by the results.

The networks that treat this as a wake-up call will earn disproportionate budgets. The ones that don't will find themselves stuck in the middle, watching brands walk past their buffet station and wondering where their own next meal will come from.

The full 2026 P2PI Retail Media Ratings study is available to P2PI members.

More from me on this topic:

- The Other Side of the Story: Why Retailers Struggle with Media Measurement & Standardization

- The Retail Media Performance Gap Is Even Wider Than We Thought

- The Retail Media Doom Loop

THIS WEEK

With ~83% of US retail sales still happening in physical stores, in-store retail media is finally getting the attention it deserves—and the infrastructure to match. US in-store retail media ad spend is projected to reach $1.07B by 2029 as the channel becomes more buyable, more measurable, and more like DOOH with retail data layered on top.

But there's a bifurcation happening in execution. On one side: scalable, programmatic placements—digital screens at checkout, entrance zones, endcaps, in-store audio—that brands can now buy and manage with increasing ease. On the other: experiential activations that go beyond efficiency to create something memorable and brand-building.

In this LIVE session, I'll sit down again with Jordan Witmer (Salt XC) to explore both sides of the opportunity.

We'll discuss:

* What's working now: Real examples of in-store activations from Salt's experiential and shopper work—showing the range of what brands are doing in retail environments

* Scalable vs. experiential: Where growth is concentrating, and when brands should push beyond programmatic placements into bigger swings

* Bringing social content in-store: How brands can translate their influencer-driven creative into physical retail environments

* The resilience factor: Why in-store retail media may be uniquely insulated from some of the disruption facing onsite and offsite channels (including agentic commerce)

We'll take live Q&A—bring your questions!