Researchers studying fireflies discovered something counterintuitive about standing out. When male fireflies flash in sync, females respond 80% of the time. When each male tries to outshine the others with staggered, asynchronous signals, female response drops to 3%. Synchrony evolved because it cuts through visual clutter—a system working together beats individuals competing for attention.

Dave Glaza thinks retail media has a synchrony problem.

Glaza runs DIGITS, an agency straddling both sides of the retail media divide—helping major CPGs execute retail media campaigns, while also operating retail media networks on behalf of regional grocers like Schnucks and Coburn's. That dual vantage gives him a unique perspective.

His argument, which he outlined on a recent episode of the ‘Beyond the Shelf’ podcast with Dave Feinelib, is that brands who ignore regional retail media networks are ignoring where a huge chunk of shopping actually happens.

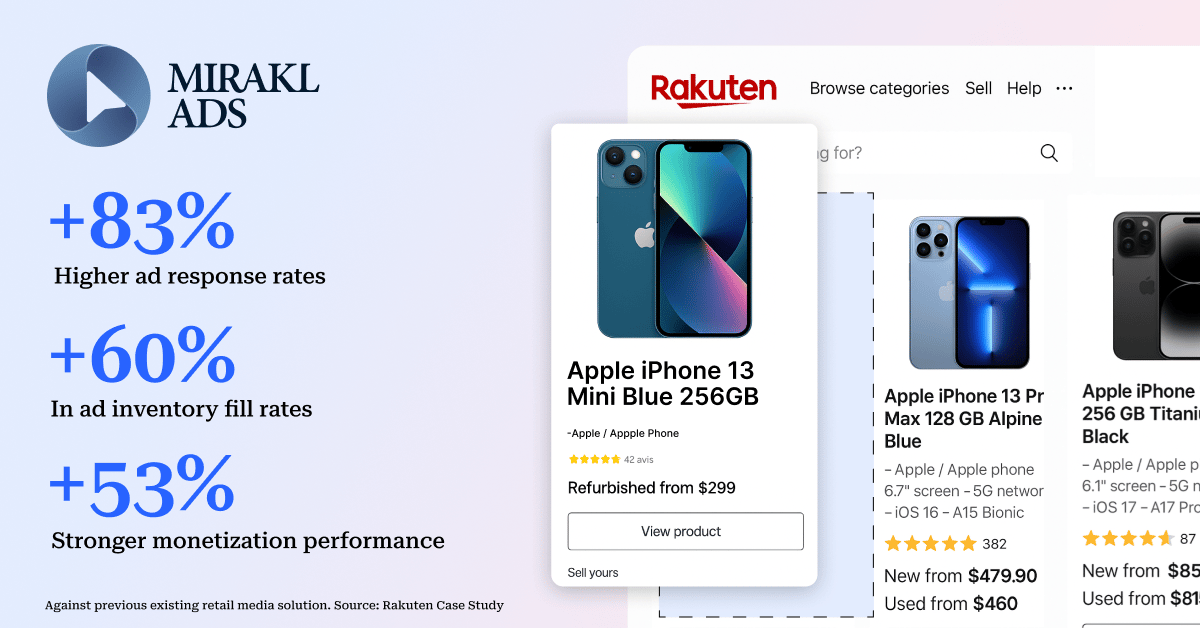

SPONSOR: MIRAKL ADS

Did you know leading retailer media networks drive 85% of their ads revenue through mid- and long-tail advertisers?

Mirakl Ads provides full funnel ad formats tailored to both 1P and 3P advertisers, leveraging unique AI-capabilities that provide unprecedented levels of relevance and engagement.

Retailers who want to capture ad spend from the long tail of 3P marketplace sellers use Mirakl Ads in their tech stack.

The Operational Ceiling Is Real

I've written extensively about why brands hit a wall at five or six retail media networks. The ANA data backs this up—55% cite lack of standardization as their top challenge.

From my agency days, my view is that managing network #11 requires nearly as much infrastructure as network #5, but delivers a fraction of the reach.

But Glaza says that brands should talk to all customers that buy their product, not just the top retailers. There is a lot of business to be won in the mid-market and regional stores.

Take Schnucks, a St. Louis grocer competing head-to-head with Walmart in their market. A brand might spend several multiples more on Walmart's RMN in that DMA than they would with Schnucks—even when both split market share roughly evenly.

"You're literally walking away from half the town," Glaza said in the podcast interview.

The Shopper Marketing Continuity

Glaza's background as a Target merchant shapes his thinking. He spent 15 years on the retail side, and that informs his critique of how centralized retail media teams operate.

His argument: if a CPG sales team would happily buy an endcap at a regional grocer, why wouldn't they buy a sponsored product placement? Both move units. The work isn't fundamentally different.

"Are they only interested in buying checklane placements at the top five retailers?" he asked. "That doesn't make sense."

But treating sponsored products as "just another endcap" undersells what sophisticated retail media can deliver—closed-loop attribution, mid-flight optimization, incrementality measurement. If regional players stick to running basic placements, they may not offer equivalent capabilities. There’s a cost to delivering an advertising offering that can compete with the sophisticated capabilities that the Amazons and Walmarts of the world now offer. This is the challenge that Glaza attempts to solve for regional players.

A Services-Led Workaround

In my previous posts on the various models of retail media alliances and consortiums, I covered:

- Tech platforms (Instacart's Carrot Ads, Best Buy's platform ambitions)

- Data federations (Rippl/Bridg's consortium model)

DIGITS Agency represents a third approach: the services-led consortium.

Realizing that brands weren’t building the internal teams or systems to solve for the fragmentation problem, Glaza built a services layer. The model works like an add-to-staff function. DIGITS co-brands with retailers (Coburn's DIGITS Retail Media Network, for example), integrates with whatever tech stack exists, and provides the sales, campaign management, and reporting capabilities that regional grocers can't justify building internally.

For regional grocers, DIGITS sidesteps the retail media doom loop I've written about—where retailers can't attract revenue without investment, but can't justify investment without revenue. For brands, it routes activation through sales teams and broker networks already calling on these accounts.

But the consortium model is not without its challenges. I've documented how even well-intentioned federations risk commoditizing retailer advantages. Some industry leaders worry that these models will primarily benefit the convening organizations rather than participating retailers, potentially commoditizing retailer advantages in favor of tech platform profits. One industry insider I spoke with drew parallels to what happened when publishers embraced programmatic advertising: “They were all decimated and commoditized, and all the value accrued to the walled gardens and tech players."

Where I Land

I've argued that 200+ retail media networks is unsustainable. That hasn’t changed.

But Glaza's challenge sticks: brands already have salespeople, shopper marketers, and broker networks managing these relationships. They're negotiating promotional windows and funding displays every week. The infrastructure exists—it's just siloed away from retail media teams.

The answer probably isn't forcing regional spend through centralized teams. It's recognizing that local activation can flow through functions that already own those relationships.

That doesn't solve the measurement gap, and it doesn't create the standardization brands demand. But it might be more realistic than expecting brands to staff up teams capable of managing 40 networks.

The fireflies figured out that synchronized signals cut through noise. Regional retail media's survival might depend on similar coordination.

Listen to the full interview on the Beyond the Shelf podcast